The International Integrated Reporting Council (IIRC) developed the Integrated Reporting (IR) framework to guide organisations in producing concise, meaningful reports that explain how they create value in the short, medium, and long term.

IR provides a framework for combining financial and non-financial information to give a holistic view of such value creation, connecting financial, environmental, social, and governance information into a cohesive story for investors and stakeholders.

Key principles and focus areas

Integrated Reporting is built around seven guiding principles:

- Strategic focus and future orientation – Reporting should explain how strategy relates to the organisation’s ability to create value over time.

- Connectivity of information – Disclosures should show relationships between financial and non-financial factors.

- Stakeholder relationships – Reporting should reflect how the organisation interacts with key stakeholders.

- Materiality – Focus on information that is relevant to understanding value creation.

- Conciseness – Reports should be clear and avoid unnecessary detail.

- Reliability and completeness – Information should be accurate, balanced, and comprehensive.

- Consistency and comparability – Enables evaluation of performance over time and against peers.

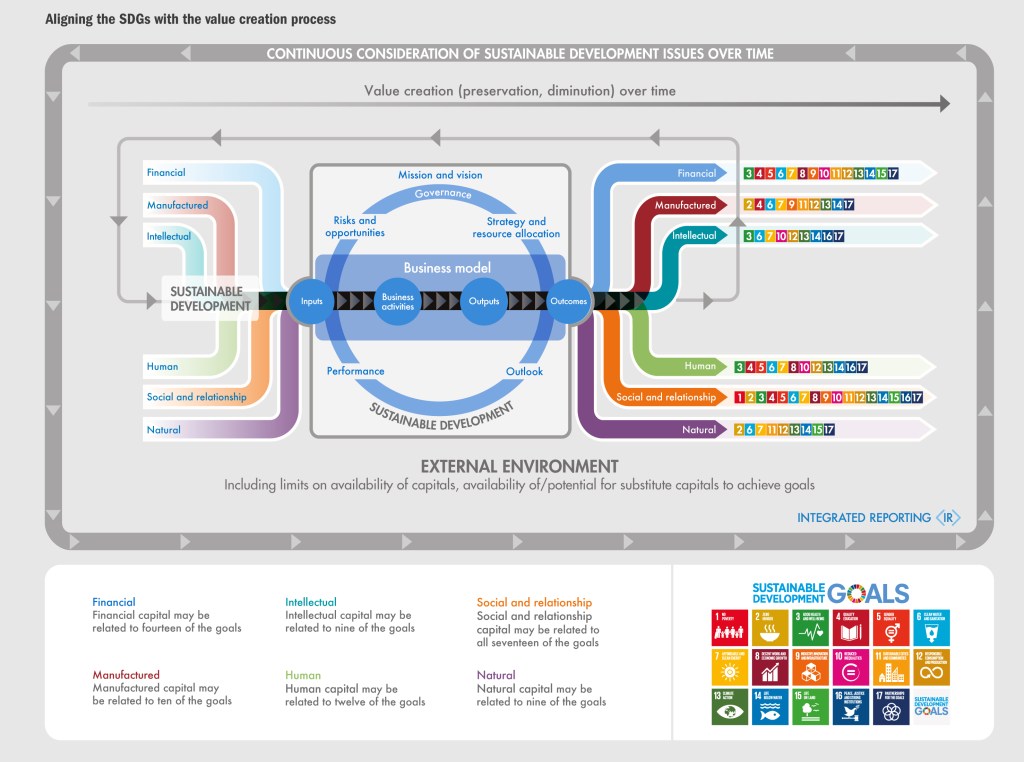

IR encourages organisations to consider six types of “capitals” in their reporting: financial, manufactured, intellectual, human, social and relationship, and natural. This framework helps illustrate how multiple resources contribute to long-term value creation.

Practical application

Implementing IR involves identifying material issues, connecting them to strategy and performance, and presenting the information in a clear, integrated report. Organisations often align IR with other frameworks such as GRI for broader sustainability reporting, SASB for industry-specific metrics, and TCFD for climate-related financial disclosures.

In this context, integrating the United Nations Sustainable Development Goals (SDGs) further strengthens the framework by linking organisational value creation to globally recognised sustainability priorities. This alignment enables organisations to demonstrate how their strategy and performance contribute to environmental and social outcomes, while enhancing materiality, stakeholder relevance, and the overall connectivity of financial and non-financial information