Over the past decade, sustainability reporting has shifted from voluntary narrative disclosures to increasingly standardized, investor-focused frameworks. At the center of this transformation is the transition from the Task Force on Climate-related Financial Disclosures (TCFD) to the International Sustainability Standards Board (ISSB).

The publication of IFRS S1 and IFRS S2 in 2023 marks a pivotal moment: the move toward a global baseline for sustainability-related financial reporting. These standards do not replace TCFD outright—they build on and absorb it, while expanding scope, rigor, and comparability.

The Legacy of TCFD

The TCFD, established in 2017 by the Financial Stability Board, created the first widely adopted framework for climate-related financial disclosures. It introduced the now-familiar four pillars:

- Governance

- Strategy

- Risk Management

- Metrics & Targets

These recommendations became the de facto global standard, widely endorsed by companies, regulators, and investors.

However, TCFD had limitations:

- It was principles-based and voluntary

- It focused only on climate

- It lacked detailed, enforceable requirements

The Emergence of ISSB

The ISSB was created under the IFRS Foundation to address fragmentation in sustainability reporting. Its goal is to establish a consistent, comparable, and decision-useful disclosure framework for global capital markets.

In 2023, the ISSB issued its first two standards:

- IFRS S1 – General Requirements for Disclosure of Sustainability-related Financial Information

- IFRS S2 – Climate-related Disclosures

These standards:

- Fully incorporate TCFD recommendations

- Provide a global baseline for sustainability disclosures

- Are designed for use alongside financial statements

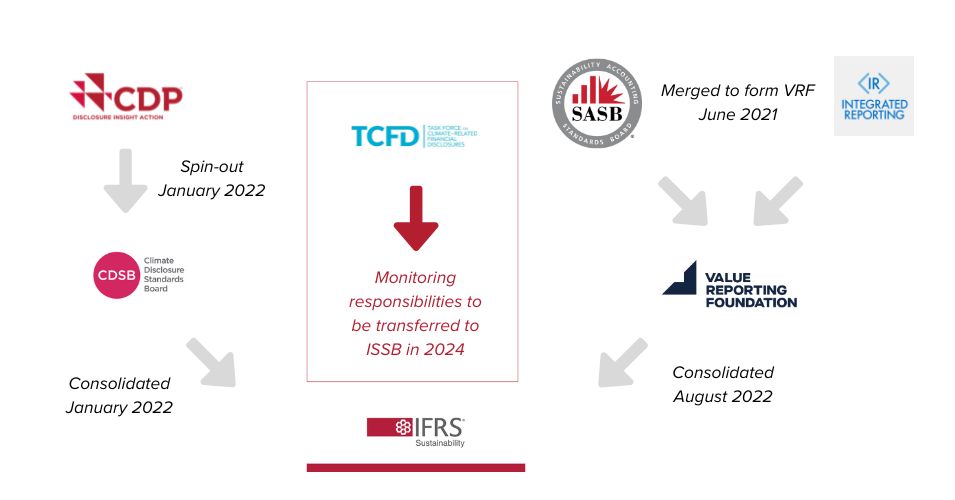

Crucially, the Financial Stability Board transferred responsibility for monitoring climate disclosures from TCFD to the ISSB, signaling the formal transition of authority .

Key Shift: From TCFD to ISSB

The transition from the TCFD to the ISSB reflects a fundamental shift in sustainability reporting. Under the TCFD, organizations followed voluntary, principles-based recommendations, whereas the ISSB introduces structured and enforceable standards that are designed to be integrated directly into financial reporting systems.

This shift also expands the scope of disclosures: while the TCFD focused solely on climate-related issues, the ISSB goes further by combining climate-specific requirements under IFRS S2 with a broader sustainability framework under IFRS S1.

In addition, the ISSB addresses the long-standing fragmentation in ESG reporting by consolidating several existing frameworks, including TCFD, CDSB, and SASB, thereby reducing complexity and improving consistency across disclosures. Finally, there is a clear move away from purely narrative reporting toward decision-useful information, with a strong emphasis on financial materiality—ensuring that disclosed sustainability information is directly relevant to investors and its impact on enterprise value.