Sustainability reporting is rapidly becoming part of mainstream financial reporting, and the introduction of International Sustainability Standards Board IFRS S1 and S2 marks a decisive shift. These standards sit within the broader system of IFRS, or International Financial Reporting Standards, which are globally used accounting rules that guide how companies prepare financial statements. These standards reshape how companies explain risk, performance, and long-term value.

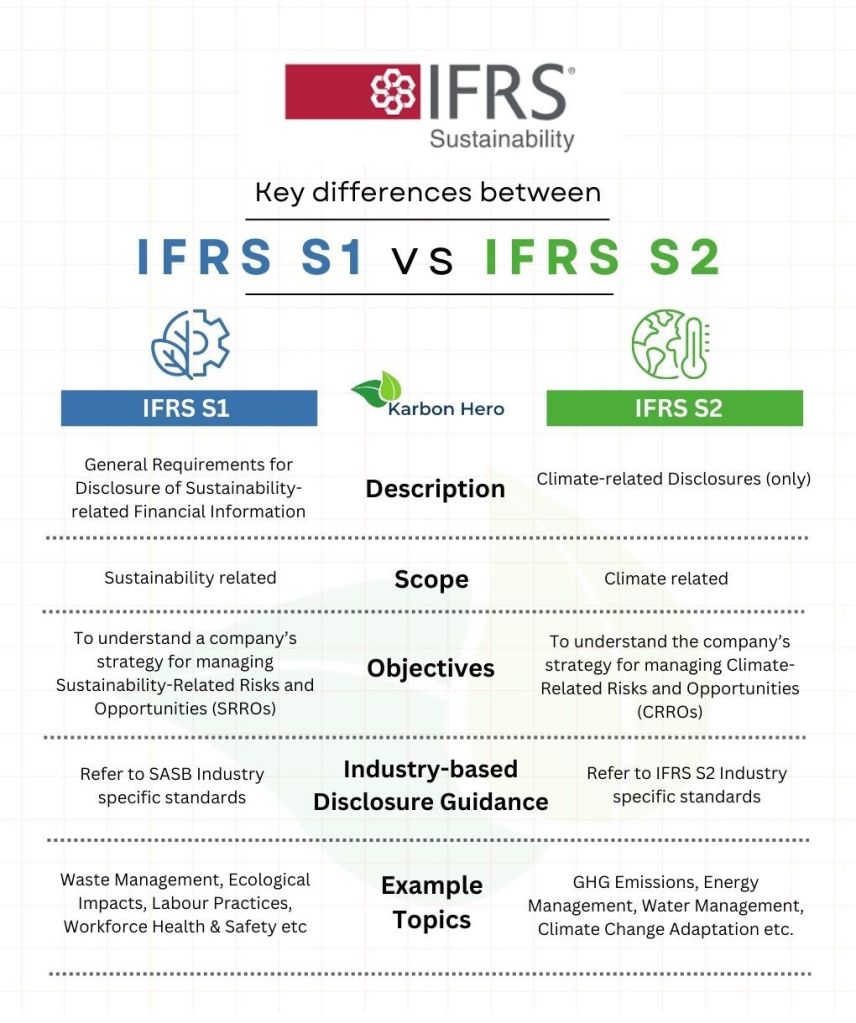

IFRS S1

IFRS S1 establishes the general framework for disclosing sustainability-related financial information. Its central concept is financial materiality, which refers to information that could influence investor decisions by affecting enterprise value. This moves sustainability reporting closer to financial accounting, where relevance and reliability are critical.

The standard requires companies to disclose risks and opportunities across short, medium, and long-term horizons. It also introduces discipline in how information is prepared, ensuring consistency with financial statements. Governance, strategy, risk management, and metrics form the structural backbone, reflecting earlier frameworks but with more precision.

Exploring IFRS S2 and climate disclosures

IFRS S2 focuses specifically on climate-related risks and opportunities. It builds directly on the legacy of the Task Force on Climate-related Financial Disclosures, but adds more detailed and enforceable requirements. Climate is treated as financially relevant, not just environmentally important.

A key technical feature is the requirement to disclose greenhouse gas emissions across Scope 1, Scope 2, and Scope 3. Scope 1 covers direct emissions, Scope 2 relates to purchased energy, and Scope 3 includes value chain emissions. This creates a more complete picture of a company’s climate exposure.

How the two standards work together

IFRS S1 and IFRS S2 are designed as a connected system rather than standalone rules. IFRS S1 provides the general principles and structure, while IFRS S2 applies those principles specifically to climate. This modular approach allows additional topics to be added over time without redesigning the entire framework.

The standards also draw from established guidance such as the Sustainability Accounting Standards Board and the Greenhouse Gas Protocol. This integration reduces fragmentation and supports comparability, which has long been a challenge in sustainability reporting.

Why these standards matter in practice

The introduction of IFRS S1 and IFRS S2 signals that sustainability information is becoming part of core business reporting. Companies must now connect environmental and social factors to financial outcomes, requiring stronger data systems and internal controls.

This shift also changes how professionals approach analysis. Financial analysts, accountants, and sustainability specialists increasingly work with the same datasets, interpreting how non-financial risks translate into financial performance. The result is a more integrated view of corporate value.

The development of these standards continues to evolve, with jurisdictions adopting and adapting them at different speeds, and with new guidance likely to expand their scope over time.