Materiality is a cornerstone concept in sustainability reporting, yet it is often misunderstood or oversimplified. In the context of ESG and climate reporting, materiality helps organisations determine which issues are significant enough to influence decisions made by stakeholders. This concept is critical for preparing meaningful and focused disclosures that are both credible and decision-useful.

What materiality means

Materiality refers to the importance or relevance of an issue to stakeholders, including investors, regulators, employees, customers, and communities. In practical terms, a material issue is one that could affect the organisation’s performance, strategy, or reputation. For example, for a manufacturing company, energy efficiency and emissions may be highly material, while social diversity metrics may be more critical for a service-oriented business.

Financial vs. double materiality

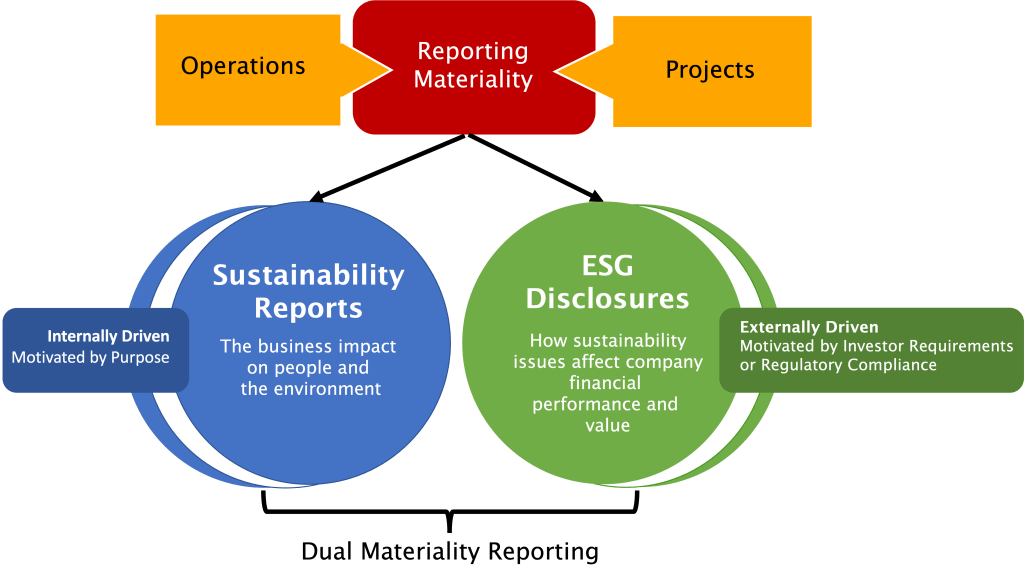

There are two main perspectives on materiality in sustainability reporting. The financial materiality lens focuses on ESG factors that can influence enterprise value or financial performance. This approach is commonly used in frameworks like TCFD, SASB, and ISSB.

In contrast, double materiality expands the scope to include impacts that the organisation has on the environment and society, regardless of immediate financial implications. GRI and the EU CSRD adopt this broader perspective. Understanding both approaches is important when selecting reporting frameworks and determining which data to collect and disclose.

How materiality is assessed

Materiality assessment is a structured process that combines research, stakeholder engagement, and internal analysis. Organisations typically identify potential ESG topics, evaluate their significance to internal and external stakeholders, and prioritise those with the highest impact or risk.

Techniques include surveys, interviews, workshops, and quantitative risk assessments. Visual tools such as materiality matrices can help map issues by their relative importance and influence on decision-making.

Once material issues are identified, organisations use them to guide strategy, risk management, and reporting. Materiality informs which KPIs, metrics, and targets to track and disclose. It also helps focus resources on areas with the greatest strategic or societal impact, supporting both compliance and stakeholder trust.